Compare Cashback Credit Cards | Find the Best Deals Today

- Jan 6

- 12 min read

When you're trying to compare cashback credit cards, it all comes down to one thing: matching the card's rewards to your actual spending habits. It's easy to get drawn in by a big headline rate, but the best card isn't always the one that shouts the loudest. The real value comes from figuring out whether you'll earn more from a simple flat-rate cashback on every single purchase or from a card that offers much higher tiered rewards in specific areas, like your weekly grocery shop or filling up the car.

That choice right there is what separates getting a little bit back from getting a lot back.

Finding Your Best UK Cashback Credit Card

Let's be clear: picking the right cashback credit card is a very personal decision. The best card for your friend might be a terrible choice for you. It all depends on your unique spending, whether you're comfortable paying an annual fee, and if you tend to clear your balance every month. Before we jump into the side-by-side details, it’s vital to have a clear idea of what you’re looking for.

The UK credit card scene is incredibly competitive right now, which is great news for us consumers. Lenders are rolling out some fantastic promotional deals to win new business. In fact, new credit card applications shot up by 19% in a single year, and a huge chunk of that was driven by people chasing valuable perks. What's really telling is that 50% of those new cards came with promotional terms like cashback bonuses. This signals a perfect opportunity to snag a rewarding deal. You can dig into these market trends in more detail in Equifax's latest report.

Core Decision-Making Factors

To cut through the noise, focus on these three things:

Reward Structure: Look at your bank statements. Would you genuinely earn more from a straightforward flat-rate card (e.g., 0.5% on everything) or one with higher rates in specific categories you spend a lot on (like 3% on groceries or fuel)?

Annual Fees: A card with no annual fee is often the simplest and safest option. That said, if you're a big spender, a card with a fee could offer such high rewards that you end up with more cash in your pocket, even after the fee is paid.

Sign-Up Bonuses: These introductory offers can provide a nice initial boost, but don’t let a flashy bonus distract you. Make sure the card’s long-term earning power still aligns with your spending after the honeymoon period is over.

The goal is to find the structure that pays you the most for the spending you already do. This strategic mindset is key to turning everyday expenses into tangible rewards.

To help you see how these factors look in the real world, here’s a quick overview of some popular card types.

Quick Card Comparison At a Glance

Here is a summary table to give you a feel for how different cards stack up against each other based on these key features.

Card Name | Cashback Rate | Annual Fee | Introductory Offer | Best For |

Card A | 1% flat-rate | £0 | £20 cashback after £500 spend | Everyday spenders seeking simplicity. |

Card B | 3% on groceries, 1% elsewhere | £30 | 5% cashback for the first 3 months | Families with high grocery bills. |

Card C | 0.75% flat-rate, no foreign fees | £0 | None | Frequent travellers who want rewards. |

This table shows how quickly the "best" card changes depending on your priorities—whether that's simplicity, maximising a specific spending category, or avoiding fees while abroad. Now, let's dive deeper into the top contenders on the market today.

How UK Cashback Cards Actually Work

Before you can properly compare cashback credit cards, it helps to get your head around how they actually put money back in your pocket. At its heart, cashback is just a simple rebate on your spending. But the devil is in the detail, and card providers have come up with a few different ways to structure these rewards.

The way a card calculates what you earn is genuinely the most important factor in figuring out if it’s the right one for you. Most UK cashback cards follow one of three main models, each designed for a different kind of spender. The trick is to match the card’s model to your own financial habits.

The Main Cashback Models

First up is the most common and straightforward option: the flat-rate cashback card. These cards give you a single, fixed percentage back on almost every pound you spend, no matter where you spend it. Think of a card that offers 0.75% back on everything, from your morning coffee to your monthly direct debits.

The beauty of a flat-rate card is its simplicity. You don't have to juggle different cards for different shops or worry about bonus categories. This makes it a fantastic choice if you value an easy life or if your spending is spread thinly across many different areas.

On the other side of the coin, you have bonus category cards. These cards dangle much higher cashback rates for spending in specific areas. For instance, a card might offer a tempting 3% on groceries and fuel but a standard rate of just 0.5% on all other purchases. They’re built for people who know exactly where their money goes each month.

Understanding the mechanics here is key. A bonus category card can deliver fantastic returns, but only if its bonus categories align with where you actually spend most of your money. If they don't, you'll often find a simple flat-rate card earns you more over the course of a year.

Introductory Offers and Tiered Systems

Finally, lots of cards use introductory rates to grab your attention. These are short-term promotions that give you a seriously boosted cashback rate, like 5% on everything you buy for the first three months. It's a great way to earn a quick, chunky reward, but you must look past the initial dazzle and assess the card’s long-term value after the offer ends.

Some cards also operate a tiered system, where your earnings rate climbs once you hit a certain spending milestone. For example, you might earn 0.5% on the first £5,000 you spend in a year, which then jumps to 1% on everything above that. This structure is designed to reward bigger spenders. Getting to grips with these different models is the essential first step to choosing the right cashback card for you.

A Detailed UK Cashback Card Comparison

Right, let’s get into the nitty-gritty. Now that we've covered the basics of how cashback works, it’s time to put the top UK cards under the microscope. This is where we look past the flashy headlines and dig into the small print that really makes a difference to your wallet.

Choosing the right card often comes down to fine margins. A seemingly tiny difference of 0.25% cashback might not sound like much, but when you're talking about thousands of pounds in spending over a year, it really starts to add up. An annual fee can feel like a waste of money, but for the right person, it can unlock rewards that far outweigh the cost.

Evaluating Cards Based on True Value

To see how this works in practice, I’ll break down three popular types of cashback cards you’ll find on the market. Let's call them the "Everyday Earner," the "Supermarket Specialist," and the "Premium Performer." Each one is tailored for a different kind of spender, so understanding their unique strengths is the key to making a smart decision.

These cards are more popular than ever. Recent figures from the FICO UK Credit Card Market Report show the average monthly credit card spend has climbed to £825—that's an 11.8% jump month-on-month. Rewards are a big reason why, but it’s a good reminder to manage your balance carefully.

To do a proper comparison, we need to look at the whole picture. That means dissecting everything from the welcome bonus and annual fee to the redemption rules and the representative APR. This way, you can see how a card truly stacks up against your own spending habits.

In-Depth Feature and Fee Breakdown

The table below lays out the crucial details for our three example cards. When you look at it, pay special attention to how things like annual fees and foreign transaction fees can chip away at what you earn.

Card Feature | Card A Details | Card B Details | Card C Details |

Cashback Rate | Flat 0.75% on all spending | 3% on groceries & fuel, 0.5% elsewhere | Tiered: 1% up to £10k, 1.25% after |

Annual Fee | £0 | £25 | £95 |

Welcome Offer | £25 cashback when you spend £1,000 | 5% cashback for first 3 months (cap £100) | £50 cashback after £3,000 spend |

Redemption | Automatic annual credit | Manual redemption via online portal | Can be redeemed as credit or gift cards |

Foreign Fees | 2.99% on non-sterling transactions | 2.95% on non-sterling transactions | 0% on non-sterling transactions |

Representative APR | 24.9% (variable) | 26.9% (variable) | 21.9% (variable) |

As you can see, there’s no single "best" card—it all depends on you. The Everyday Earner is a simple, safe bet for anyone who dislikes fees and has varied spending. For families with a hefty grocery and fuel bill, the Supermarket Specialist's high bonus rate can easily make the modest annual fee worthwhile.

Here's a key takeaway: an annual fee isn't automatically a deal-breaker. For a big spender, the Premium Performer could easily be the most profitable card. If you spend £20,000 a year, you’d earn £225 back. After the £95 fee, you’re left with a net gain of £130—a good bit more than the £150 you'd earn with the fee-free Everyday Earner.

Situational Analysis and Best Use Cases

So, how does this translate into real life? Let's match these cards to different people.

The Everyday Earner: This is the perfect "set it and forget it" card. With no annual fee and a simple flat rate, you don't have to think about spending categories. You just spend and earn.

The Supermarket Specialist: If your monthly budget is dominated by the big weekly shop and filling up the car, this card is designed for you. Its power comes from that high bonus rate on specific categories. For more guidance on choosing the right card, our guide on the 15 best credit cards in 2025 is a great place to start.

The Premium Performer: This card is a brilliant fit for two types of people: high spenders and frequent travellers. The tiered rate rewards you for spending more, and the 0% foreign transaction fees can save you a small fortune on overseas purchases, making that annual fee a savvy investment.

At the end of the day, the goal is to find a card that rewards your existing lifestyle, not one that tempts you to spend more. Take a good look at your bank statements, compare them against these features, and you’ll be able to pick a card that delivers real value, year after year.

Aligning a Card with Your Spending Habits

The best way to sort through the noise of cashback offers is to stop focusing on advertised rates and start looking at your own bank statements. The true worth of any cashback card isn't what it could earn, but what it will earn based on your actual, everyday spending. Let's dig into how to match a card to your life, not the other way around.

To make this real, we'll walk through a couple of common examples. This shows you exactly why the perfect card for your neighbour might be a terrible choice for you. It's about moving from a simple list of features to a practical decision that puts more money back in your pocket.

The Weekly Supermarket Shopper

Picture a family whose biggest monthly expenses are the weekly food shop and keeping the car topped up. A typical month for them might look like this:

Groceries: £500

Fuel: £150

Other Spending (utilities, subscriptions, etc.): £350

For this family, a bonus category card that gives extra cashback on groceries and fuel is the obvious front-runner. If that card offers 3% back on those two categories, they'd earn a respectable £19.50 just from the supermarket and petrol station (£500 + £150 = £650 x 0.03).

Assuming the card pays 0.5% on everything else, they'd add another £1.75 from their other spending. That brings their total monthly cashback to £21.25. In contrast, a simple flat-rate card offering a blanket 0.75% on their total £1,000 spend would only net them £7.50. That’s a huge difference over a year.

The Digital Subscriber and Varied Spender

Now, let's think about a young professional whose spending is spread all over the place. Their budget is a mix of modern essentials and lifestyle costs.

Subscriptions (Streaming, Software): £80

Dining and Entertainment: £250

Public Transport/Ride-Sharing: £120

Other Retail Spending: £400

This person doesn't have one or two standout spending categories, which makes a bonus card tricky to get the most out of. A flat-rate card offering a consistent 0.75% or 1% on every single purchase is a much smarter, simpler choice. On their total monthly spend of £850, a 1% flat-rate card delivers a clean £8.50 back, with zero effort spent tracking categories.

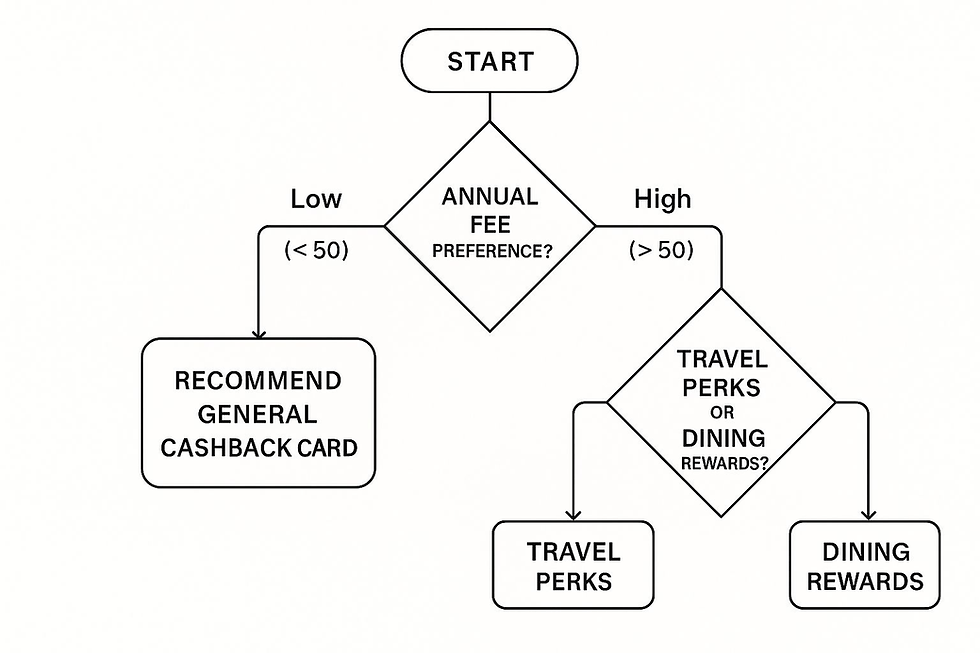

This image can help you quickly figure out which path makes the most sense for you at a glance.

As you can see, the first big question to answer is often whether you’re willing to pay an annual fee to unlock higher rewards.

The real secret is this: Don’t pick a card and try to change your spending to fit its rules. Pick the card that rewards you most for the spending you already do. Your bank statement is the ultimate cheat sheet.

Getting smart about your credit card is just one piece of the puzzle. This same approach of analysing your spending works for all your major outgoings. That’s why we also created an expert guide to help you save money on car insurance. When you know where your money is going, you can make choices that actively reward you.

Navigating the Hidden Costs of Cashback Cards

Getting cash back on your spending feels great, but that's only half the story. The real win is actually keeping those rewards, and that takes a bit of financial discipline. It's all too easy to fixate on the shiny cashback rates and forget about the hidden costs that can quickly turn a great card into a financial headache.

Let’s be clear: the golden rule of using any rewards credit card is to pay your balance in full and on time, every single month. If you don't, you'll watch your hard-earned cashback get gobbled up by interest charges that are almost certainly higher than what you earned.

How Interest Charges Can Erase Your Rewards

Here’s a quick, real-world example. Say you get a card offering a decent 1% cashback on everything. You spend £1,500 in a month, which nets you a tidy £15. Not bad.

But if you only make the minimum payment and let the rest of the balance roll over, the interest kicks in. On a card with a typical 24.9% APR, the interest you pay in just one month could easily be more than the £15 you earned. Your reward is gone, and you’re now paying the bank for the privilege.

The real trap is that the buzz of earning rewards can tempt you into spending a little more than usual, making the balance harder to clear. When you're comparing cards, the APR is just as important as the cashback rate—especially if you think there’s even a small chance you might carry a balance.

Other Costs to Watch Out For

Interest isn't the only thing that can chip away at your cashback. You need to keep an eye on other fees too.

Annual Fees: A card with an annual fee only makes sense if you spend enough for the cashback to comfortably cover that fee and still leave you with a profit. Always do the maths first.

Foreign Transaction Fees: If you travel or buy from overseas websites, these fees—often around 3%—can be a killer. A dedicated fee-free travel card could save you more on one trip than your cashback card earns you all year.

Here in the UK, we've seen how rewards can fuel spending and, unfortunately, contribute to debt. Total outstanding credit card debt recently hit £71.7 billion, a 9.5% jump in just one year. With the average household holding £2,486 in credit card debt, it's a stark reminder of the risks of chasing rewards without paying off the balance. You can read more about these credit card statistics on MoneySuperMarket.

Ultimately, being disciplined isn't just good advice—it's the only way to make cashback work for you. For those looking to give their finances an extra boost, check out our quick-start guide for earning extra income.

Common Questions About Cashback Cards

Even after you've weighed up the options, a few practical questions can linger. Getting these sorted is often the last step you need to pick a card with confidence and start using it smartly. Let's dig into some of the queries I hear most often.

Does My Credit Score Matter?

Absolutely. Your credit score is one of the most important factors for lenders. The top-tier cashback cards—the ones with the best rates and big sign-up bonuses—are usually reserved for people with ‘Good’ to ‘Excellent’ credit scores. A solid credit history proves you're a dependable borrower.

If your score isn't quite there yet, don't worry. You can still find cashback cards, but they might offer a lower rewards rate, a smaller credit limit, or a higher APR. It’s always a good idea to know your score before you start applying so you can focus on cards you're likely to get.

Is One Card Better Than Several?

This really comes down to your own spending habits and how organised you are. For pure simplicity, a single, high-quality flat-rate card is tough to beat. You earn the same on everything, so there's no need to think about which card to pull out of your wallet. It's effortless.

On the other hand, if you're willing to put in a little more work, a strategy called ‘card stacking’ can seriously boost your returns. This means using different cards for different things—one for your weekly shop, another for petrol, and a third for your holidays. The trick is to make sure any annual fees don't wipe out your extra earnings and that you're on top of all the separate payments.

It’s crucial to remember that your cashback isn't always permanent. If you close your account before redeeming your rewards, you could lose them. Some issuers also have expiration dates or require a minimum balance to cash out, so always read the small print.

Is Credit Card Cashback Taxable?

In the UK, the good news is that for personal spending, the answer is generally no. Her Majesty's Revenue and Customs (HMRC) usually sees credit card cashback as a simple rebate or a discount you get after a purchase, not as income that needs to be taxed.

The situation can be different if you're earning cashback on business expenses, so it’s always best to check with a tax professional for any business-related finances. For anyone keen to build up their financial savvy, reading some of the best personal finance books can provide great insights that go well beyond just credit cards.

Comments